Photo Credit: Antara Mrinal

Clear Cut CSR Desk

New Delhi, UPDATED: Oct 01, 2025 12:42 IST

Written By: Antara Mrinal

Introduction

In India, having a Corporate Social Responsibility (CSR) Policy is no longer an issue of just corporate goodwill; it is a legal requirement. Under the Companies Act, 2013, Companies of a certain profitability, turnover, or net worth must allocate 2% of their average net profit towards social and developmental projects. Even though this provision made India the first country to legally mandate CSR spending, the less explored query is the manner in which companies report their activities, and the meaning of these reports in the context of corporate accountability and social impact. A research by Prantik Roy and Uday Krishna Mittra (2022) on ‘Corporate Social Responsibility Reporting: A Review in Indian Perspective’ published in the NUJS Journal of Regulatory Studies, sheds critical light on this issue. Covering the period 2017-2022, the authors conducted CSR reporting reviews in India and wrote about the reporting growth, sectoral concentration, methodological gaps, and other gaps which provided valuable insights. Their work not only described the state of social disclosure by Indian companies but also helped in identifying what is so clearly absent.

Key Findings

According to the research, CSR reporting and disclosures have indeed expanded in India in the last five years. Larger companies in the banking, manufacturing, IT and energy sectors tend now to routinely report on CSR matters, often combining CSR disclosures into their annual reports. These large companies primarily report on themes such as education, health, sanitation, and clean drinking water – essentially safe and non-controversial areas that resonate with the public.

Nevertheless, CSR reporting has not expanded everywhere. Firms within the agricultural and textile sectors and SMEs lag in reporting, reporting little to no information. This status of CSR reporting leads to an uneven picture of CSR in India: certain sectors seem to have moved so far ahead and actively report on CSR issues while other sectors seem not to be reporting at all, resulting in anomalies for regulators, scholars and the public when trying to build an accurate and informed understanding of CSR in India.

Methodological Concerns

The variation in both structure and methodology in reporting results in a lack of uniformity. A few of these entities facilitate reporting using internationally recognized methodologies, such as the Global Reporting Initiative (GRI). This offers a set of guidelines that incorporates standardized measures for environmental, social, and governance reporting. Others, however, create their own reporting formats designed and developed to their internal requirements or stakeholder needs. Therefore, creating a uniform and standardized set of disclosures that can be easily matched and compared for similarity and consistency is nearly impossible. One organization’s “community development” may entail the construction of a school, while another may categorize the same activity purely under “education.” Some companies emphasize the outputs of their initiatives (number of students reached), while others emphasize the outcomes (gained literacy skills). This lack of consistency may prevent organizations from comparing initiatives across industries and aggregating data to create a rational, comprehensive, and coherent national picture.

What’s Being left Out

CSR literature preferences are outlined by Roy and Mittra. Corporate disclosures mainly center on education, health, sanitation, and drinking water. These are perceived as safe, visible, and easily acceptable, and thus, as opportunities for companies to show public welfare concern. However, issues like sustainability, livelihood, skills, and gender seem to get less prioritization in disclosures. This reflects, in part, an emphasis on short-term visible projects and for many, an association of philanthropy with CSR. This perception of CSR as philanthropy focused on short-term highly visible projects is partly caused by CSR in India being compliance driven. Companies seem to care more about presenting a good image in the short term than about designing realistic, measurable, long-term plans for social change.

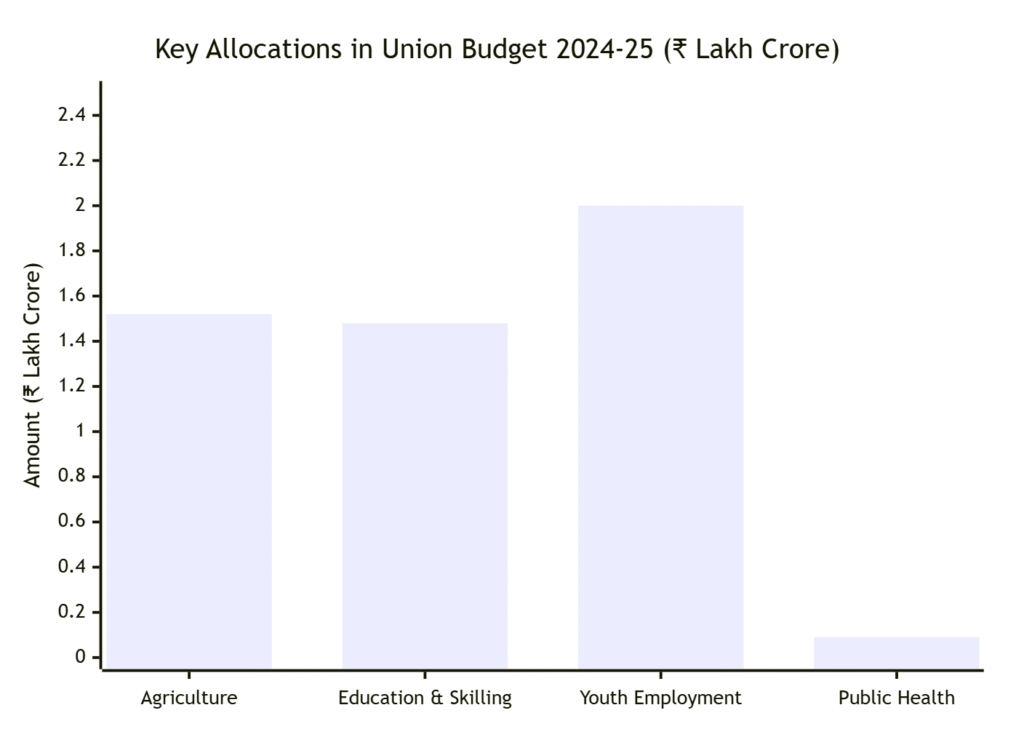

However, the Union Budget 2024-25, we see a major improvement in the skills and livelihood sector (devinsights.co.in). Livelihood, Education and Skill Development became a key thematic area. Gender, Climate and other factors still remain less favored.

Roy and Mittra identify a number of blind spots in CSR reporting in India, some of which are still ongoing. The lack of common metrics is the most concerning. Without some common metric, disclosures across companies will not be comparable and the impact will not be able to be measured. Equally concerning is the lack of stakeholder engagement in the reporting. Most of the CSR reports are written for regulators and shareholders, not explicitly for the very communities that are to get benefits from the projects. This lack of accountability, as well as the reports providing avenues for the interests and voices of marginalized communities, are less than transparent.

It is also concerning that, while reporting of CSR is on the rise, half of the economy is still engaged in underreporting. Smaller firms, as well as companies that are outside of the dominant sectors also report the least amount of information or do not report at all on CSR. At the same time this has implications for understanding the larger CSR landscape, very few companies produce substantive reflection on the challenges they face. Rarely do projects transparently describe the risks and available resources, unintended consequences, and they reconstructed all of the best parts. Reporting bouquets then simply provide happy and glossy stories about the work to make social development look less messy.

Contextualizing CSR Reporting Patterns

Roy and Mittra’s findings are consistent with other studies both in India and around the world. In the empirical investigation of CSR reporting by companies on the National Stock Exchange of India, the same authors found that public sector enterprises attained an average disclosure score of 0.52 whereas the private sector scored 0.32, highlighting variance in the quality of reporting. Internationally, there are also studies of CSR disclosures that demonstrate similarly wide disparities in how research evaluates methodology and accounting outlines. Another well-cited earlier study of CEO statements in Indian annual reports also showed that CSR narratives tend to serve an image management function rather than genuinely informing stakeholders. Therefore, all of this research provides evidence of how the challenges that Roy and Mittra encountered are neither isolated, nor short-lived. Rather they reveal systemic deficits in corporate reporting on accountability and transparency for social investments.

Implications for CSR Practices

As global investors increasingly focus on Environmental, Social, and Governance (ESG) performance, the importance of CSR reporting directly relates to capital and associated corporate reputations. If reporting is absent or inconsistent, this can undermine investor confidence, and it may further hinder the adaptation of successful social and socially responsible practices across sectors.

Conclusion

The review emphasizes the more urgent areas which merit regulatory attention for policymakers. Tighter specifications on what constitutes standardized disclosures, mandatory third-party audits, and greater stakeholder input would significantly enhance the quality of CSR reporting. For practitioners and NGOs, the intention is to provide a useful roadmap outlining areas of corporate focus and where advocacy is needed to push companies to attend to important development issues that may have been forgotten.

In the end, Roy and Mittra’s review reminds us that CSR reporting in India is still a ‘glass half full’. The legal mandate has succeeded in creating a culture of giving, but the quality of reporting is vexingly uneven, inconsistent and far too often cosmetic. In order for CSR in India to be taken from a compliance exercise to a more genuine approach for inclusive development, companies must harness the notion of reporting that is transparent, comparable, and community centered. Only then will CSR be able to begin fulfilling its original intent of closing the social gap of wealthy corporate institutions, and match their declared vision of a more equitable and sustainable India.