Early financial literacy for children in India builds lifelong money skills, promotes saving and budgeting habits, reduces debt risk, and strengthens family financial health.

I In many Indian homes, the first money lesson happens unintentionally – a child is given pocket money or plays with a parent’s coins. Yet financial literacy is the knowledge, skills, and attitudes needed to manage money. It is a learned habit that ideally should be taught, not just caught. Experts argue these habits stick best when started young. As one OECD definition notes, financial literacy isn’t just investing it includes basic saving, budgeting, planning and banking. In other words, teaching a child how to save a few coins or allocate allowance is as fundamental as teaching reading or arithmetic. Simple classroom games (like handing out play-money to simulate budgets) have shown to engage students in practical decision-making. In one U.S. school, for example, eleventh graders played a bean-based budgeting game (beans as salary units) where they chose between “buying” a bus ride or car with their beans. These fun, hands-on lessons not only capture interest, but they also pay off: teenagers who had three years of high-school finance instruction were 40% less likely to fall a month behind on credit obligations and had credit scores about 25 points higher as young adults.

More importantly, these benefits endure. A longitudinal study found that the gains from teen finance classes higher savings rates and faster debt repayment were still measurable 12 years after graduation.

Remarkably, the ripple effects extend beyond the student. In the U.S. study, parents of students who took personal-finance courses saw better outcomes: their loan-default rates fell by about a quarter, and their credit scores climbed about 5%. Even teachers notice. In Parkdale High School (Maryland), teacher Tamekia Davis saw her own savings grow after teaching budgeting games to students. These findings echo global research for example, a recent World Economic Forum analysis of a Peruvian financial-education program found parents’ loan-default probability dropped 26% after their children’s schooling. In short, early money lessons can transform whole families’ financial health.

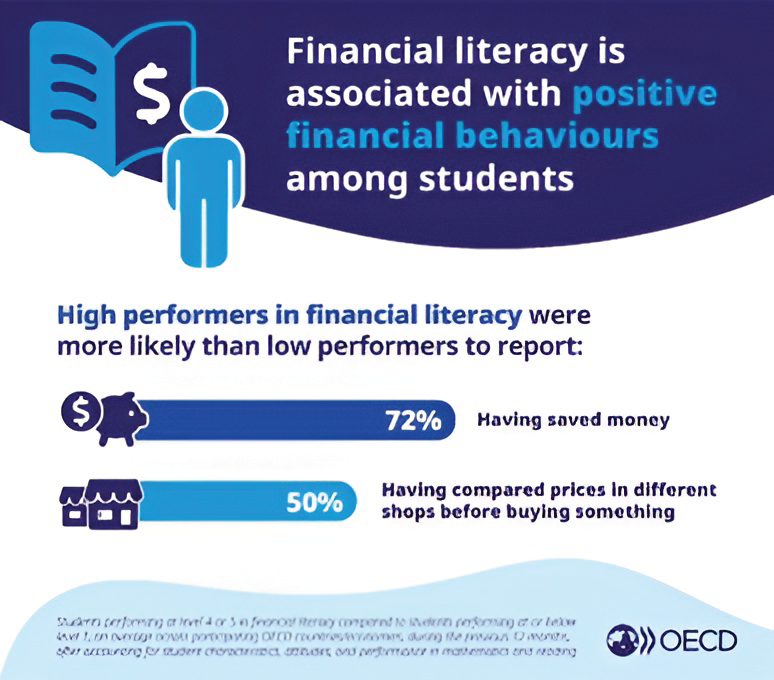

The evidence is clear that starting finance education young builds a stronger foundation. OECD’s PISA global survey of 15-year-olds shows that students who talk to parents about money score signifi-cantly higher on financial literacy tests. In fact, children who ask their parents about money do on average 27 points better on OECD assessments. This illustrates that parents are already children’s first financial teachers. An astonishing 94% of teenagers worldwide report learning about money from family members. In theory, then, educating children also educates parents. As one PISA report notes, most youths face real spending decisions (even in adolescence), so empowering them with knowledge makes them more financially resilient in shocks like a pandemic. It’s a virtuous cycle: kids who budget well at home reinforce those habits into adulthood.

Yet India’s reality falls short of these ideals. National surveys paint a worrying picture of low financial skill among all age groups. According to the 2019 NCFE–RBI survey, only about 27% of Indian adults could correctly answer basic finance questions (interest, inflation, budgeting). Even a broader RBI study in 2023 found just 62.6% of Indians met “basic financial literacy” criteria (knowl-edge, behaviour and attitude combined), well below the roughly 85% average proficiency seen among OECD 15-year-olds. These low rates coexist with wider education gaps: the ASER 2024 survey reports that 76.6% of rural Grade-3 children cannot even read a Grade-2 text, and 66.3% cannot do simple subtraction. In practice, that means most Indian children never even see money concepts in school because they are still struggling to read.

still struggling to read.Despite these hurdles, India’s youth are already a dominant economic force. A recent Snap/BCG report highlights that India’s Gen Z (about 377 million people aged 12–27) already drives roughly 43% of the country’s consumer spending. Put bluntly, almost half of the country’s market purchases are influenced by young people. Their direct spending power is projected to hit $1.8 trillion by 2035. Yet without guidance, much of this money flows into consumer debt or poor financial decisions. In fact, the World Economic Forum notes that 51% of Indian adults report difficulty meeting debt payments – well above the global average. A generation holding this much spending power without financial know-how could easily fall into “buy now, pay later” traps or high-interest debt. This gap between spending power and skill has sparked action. Recognizing the risk, India’s regulators and educators are starting to put financial education on the map. The government’s National Strategy for Financial Education (NSFE) 2020–25 explicitly targets children and youth as priority audiences. In practice, this means curriculum changes and new programs. By 2022, for example, several State Boards and the NCERT began introduc-ing financial-literacy modules into middle and high school syllabi. Even CBSE teamed up with the NSE Academy to launch an “Introduction to Financial.

Markets” vocational course for Classes IX–X, signalling that money management is becoming a recognized school subject (at least as a skill). To scale teaching capacity, the National Centre for Financial Education (NCFE) – a body set up by RBI and others – runs teacher training (the Financial Education Training Programme, FETP) to certify “Money Smart Teachers,” and annual NFLAT exams to benchmark

student knowledge. Banks and regulators also contribute like the RBI’s Financial Education Microsite offers games, comics and videos in 13 languages for schoolchildren, and its “Financial Literacy Week” raises awareness every February.

By combining storybooks and games, innovative programmes are showing how early lessons can work. In Project Nivesh (run by a Gurugram NGO), students in primary school read a tale called “Mary and the Secret of Savings” and played interactive budgeting games. After the program, 75% of participating children began using a structured budget (the classic 50/30/20 rule of needs/wants/savings) to manage their pocket money. Equally important, the program ignited family conversations: the proportion of

children who discussed savings with parents “almost every day” jumped by 37%. This case shows that even modest, localized interventions – when they engage kids with age-appropriate content – can shift attitudes. Children move from impulse spending toward planning and long-term goals (like saving for school fees), and they bring parents along. In one survey by India’s budget bank contests, over half of

children chose “education” as their main savings goal, reflecting a budding long-term mindset.

The home remains the cradle of finance lessons. Studies confirm that almost all students learn about money from parents or guardians. Yet many Indian families never openly discuss budgets or savings. A recent World Economic Forum survey noted that only about half of Indian children regularly talk about money with their parents (versus a global norm above 80%). Engaging families is therefore crucial. Simple practices help like giving a child an allowance tied to chores or asking them to help plan a small household purchase, turns daily life into finance class. Policymakers encourage such outreach like RBI-led

Financial Literacy Centres run workshops in villages, teaching adults and kids together about saving and

digital banking. Self-help groups and Across India, financial topics are still uneven in curricula: many rural and government schools simply lack finance lessons. Teacher training has begun but is far from universal.

NGOs organize parent-child finance games and booklets. When children learn a new money habit, they often nudge siblings and parents. In Peru, daughters who learned finance drove a 28% drop in family loan arrears. India too sees hints of this: for instance, teachers who have run budgeting exercises report parents telling them, “My child taught me how to use a bank app!”.

Alongside families and schools, technology is opening new doors. India’s rapid digital growth means mobile apps and games can reach kids in towns and villages. The RBI permits secure youth accounts as of July 2025, any minor (via a guardian) can open a bank account, and children 10 years or older can operate savings accounts independently. They can even receive debit cards and limited online banking (with parental oversight). This landmark rule is designed to make real-money practice part of learning. Some banks have started children’s accounts with rewards for saving. In parallel, NCFE’s Money Smart app and

RBI’s gamified lessons allow children to earn virtual coins for learning finance concepts. Even popular cartoon characters have been enlisted in India’s financial-education videos. The result is a multi-pronged ecosystem: a child might learn budgeting in class, reinforce it at home with a piggy bank, practice with a

mobile game, and then check her own savings account – all by age 12. Despite progress, gaps remain wide.

Surveys show stark urban-rural divides for example, one consolidated study found only 22% of rural adults are financially literate (versus 35% in urban areas), and women lag men by similar margins. Similarly, only about 28% of youth (18–25) met basic competency in one national survey, highlighting that

even younger people often rely on guesswork. Resources are thin textbooks with age-appropriate money lessons are scarce in Hindi and local languages. Many low-income families lack bank access or smartphones, so digital tools alone leave them out. Cultural taboos can stifle money talk – unlike OECD peers, only about half of Indian teenagers say they routinely discuss finances with family. Finally, measurement is weak, India runs few large-scale youth assessments of financial skills (NFLAT is one), so

policymakers rarely see the full picture or where to target efforts.Surveys show stark urban-rural divides for example, one consolidated study found only 22% of rural adults are financially literate (versus 35% in urban areas), and women lag men by similar margins. Similarly, only about 28% of youth (18–25) met basic competency in one national survey, highlighting that even younger people often rely on guesswork. Resources are thin textbooks with age-appropriate money lessons are scarce in Hindi and local languages. Many low-income families lack bank access or smartphones, so digital tools alone leave them out. Cultural taboos can stifle money talk – unlike OECD peers, only about half of Indian teenagers say they

routinely discuss finances with family. Finally, measurement is weak, India runs few large-scale youth assessments of financial skills (NFLAT is one), so policymakers rarely see the full picture or where to target efforts.

To bridge these gaps, experts increasingly argue for a coherent, multi-pronged strategy that works across policy, classrooms, families, and institutions rather than relying on isolated interventions. At the policy level, this means moving beyond pilots to mandating financial education from the primary grades onward, as envisioned under India’s National Strategy for Financial Education (NSFE). Recent steps-such as the CBSE’s introduction of financial market courses and the RBI’s 2025 circular allowing children aged 10 and above to operate bank accounts signal progress, but these need to be complemented by simpler KYC norms and easier access to youth-friendly banking to enable early, hands-on learning.

Within schools, curriculum design and teacher capacity are critical. Financial concepts must be embedded into existing subjects using age-appropriate, locally relevant material budgeting through mathematics problems, saving and planning through language and social science lessons, and everyday money decisions through stories and case studies. Public–private partnerships involving NCERT, NCFE, and financial regulators can help scale such content in multiple languages. At the same time, teacher training programs like the Financial Education Training Programme (FETP) need to be expanded so that financial literacy is not confined to commerce classrooms but reinforced across disciplines, supported by designated “financial literacy champions” within schools.

Equally important is family and community engagement, since children’s financial behaviours are strongly shaped at home. Structured parent–child activities such as maintaining a household budget diary or discussing savings goals at the dinner table can reinforce classroom learning. Evidence from PISA shows that students who regularly discuss money matters with parents perform significantly better in financial literacy, underscoring the need to design interventions that deliberately involve families.

Technology and product innovation can further strengthen this ecosystem. Gamified digital tools, interactive storybooks, and quizzes, particularly in regional languages can make learning accessible

even in resource-constrained settings, while youth-friendly financial products such as junior savings accounts with parental oversight allow children to practice real financial decision-making safely. Finally, sustained progress requires systematic monitoring and evaluation. Expanding assessments like NFLAT, disaggregating results by gender and location, and tracking long-term outcomes will allow policymakers to refine strategies and ensure that early financial education translates into real improvements in financial well-being over time.

Starting early with financial education is not just a nice idea – it’s backed by data. Global research consistently shows large, lasting dividends. For instance, U.S. studies find that requiring personal-finance

courses dramatically boosts future credit scores and sharply reduces delinquency rates (one analysis found students exposed to such courses for three years had credit scores ~29 points higher than peers). These effects persist long after students leave the classroom. Similarly, classroom programs in Peru

and Rwanda have shown that teaching kids to budget leads to better family saving and lower debt burdens. In India, early pilots are encouraging. Project Nivesh and others show even brief interventions make children think differently about money.

India’s youth are its greatest wealth, but only if they are also wise with money. As one expert puts it, embedding finance into schools and communities could transform a hard-to-reach adult population by

channelling education through children. By contrast, ignoring the opportunity risks millions learning bad habits (or none). Given how our young generation already dominates spending, the cost of financial mistakes could be huge – personal bankruptcies, over-indebted households, and wasted potential. In

contrast, investing a bit in every child’s money skill can pay off for decades.

Clear Cut Education Desk

New Delhi, UPDATED: Feb 23, 2026 09:00 IST

Written By: Subhanshu Jaiswal