India’s healthcare system has improved, but high out-of-pocket expenditure still puts a heavy financial burden on households. Reducing these costs through stronger public funding and broader insurance is key to achieving universal health coverage.

The Cost Behind Access

The changing face of the Indian healthcare system over the last two decades reflects a strategic intent towards institutional reforms, as reflected by the successful rollout of the National Health Mission and Ayushman Bharat. However, financial protection remains a major challenge across health systems worldwide. High out-of-pocket expenditure continues to burden households, as patients often pay directly for medicines, diagnostic services, and hospital care despite existing social protection mechanisms.

The biggest hindrance to achieving Universal Health Coverage is the financial burden on households when they seek healthcare services. The financial burden is so huge that it can be catastrophic for many households. Traditionally, out-of-pocket expenditure has been a major contributor to the overall expenditure on healthcare in India, which is unusually high compared to global averages. The financial burden acts as a hindrance to people receiving timely medical care, which results in inefficient healthcare services. To achieve Universal Health Coverage, it is important for India to move towards a system of prepaid financing.

Understanding Out-of-Pocket Expenditure

Out-of-pocket expenditure (OOPE) is a term used for those expenditures that are incurred by individuals for services that are not compensated by any insurance or government scheme. This includes expenditure on consultation fees, hospitalisation, medicines, tests, etc.

The Indian healthcare system has always depended on out-of-pocket expenditure. This has led to a high chance of catastrophic expenditure on health if a substantial part of household expenditure goes into healthcare services. According to data from the National Family Health Survey (NFHS-5) 2019-21, 47 percent of women between the ages of 15 and 49 face difficulties in arranging money for treatment. According to data from the National Sample Survey (2017-18), 17-18 percent of the population faces catastrophic expenditure on account of hospitalisations. According to data from the World Health Organization, 17 percent of the population faces catastrophic expenditure on account of hospitalisations. According to data from the World Health Organization, 17 percent of the population faces catastrophic expenditure on account of healthcare services.

Trend of Out-of-Pocket Expenditure in India

For many years, India has been among the countries with the highest dependence on household spending for healthcare. Patients and families have traditionally borne a large share of medical expenses directly, making healthcare costs a major financial burden.

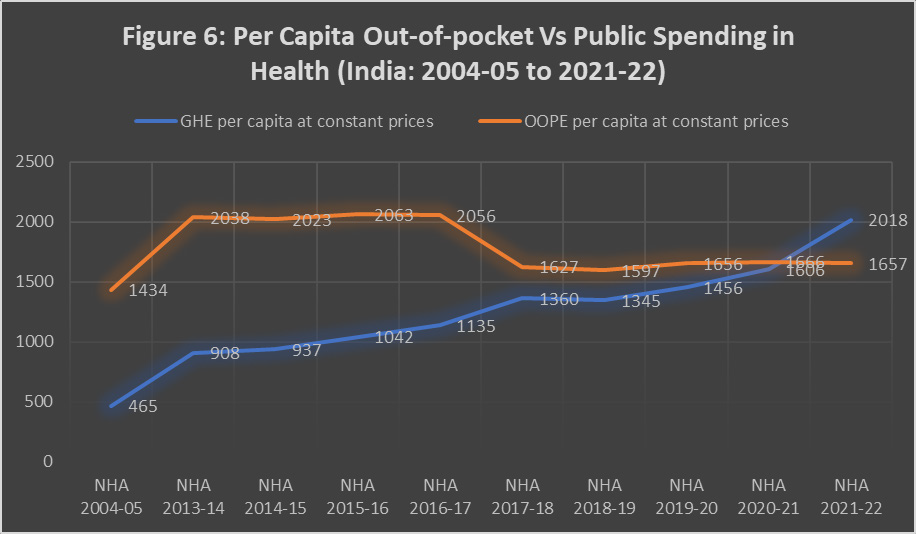

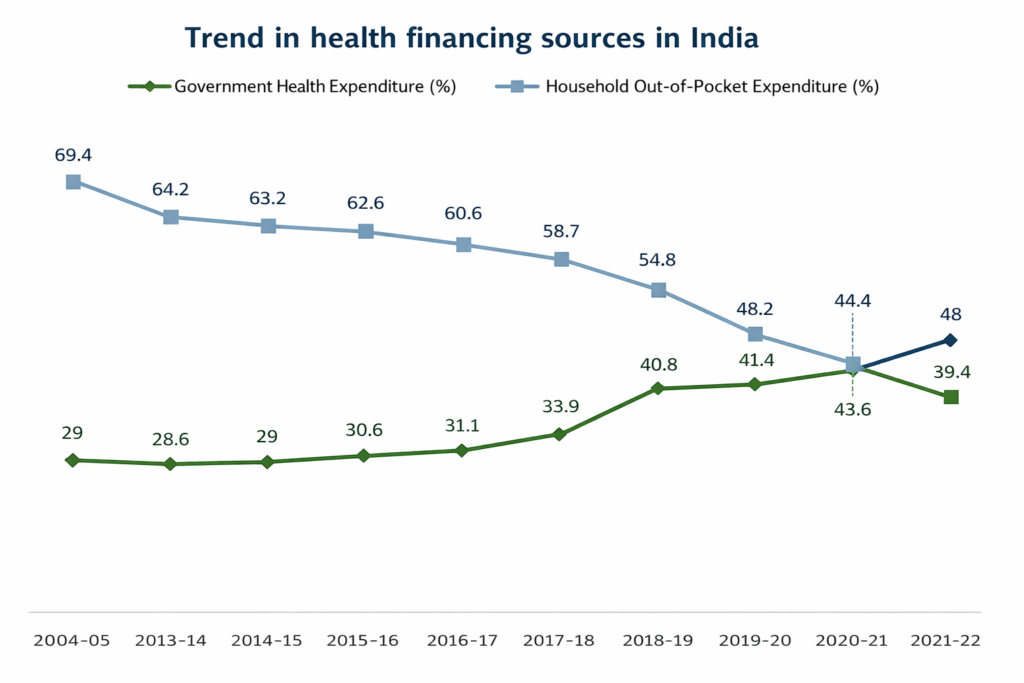

provement in this trend. According to the National Health Accounts, the share of out-of-pocket expenditure in total health spending declined from 69.4 percent in 2004–05 to 39.4 percent in 2021–22. This decline reflects increased public investment in healthcare, the expansion of government health programmes such as Ayushman Bharat, and the strengthening of primary healthcare through Health and Wellness Centres.

Despite this progress, India’s reliance on direct household payments remains high compared with many countries where out-of-pocket spending accounts for less than 20 percent of total health expenditure. Reducing financial risk from healthcare costs therefore remains an important priority for achieving Universal Health Coverage.

Composition of Household Health Spending

Understanding the composition of health spending is essential for analysing the drivers of out-of-pocket expenditure in India.

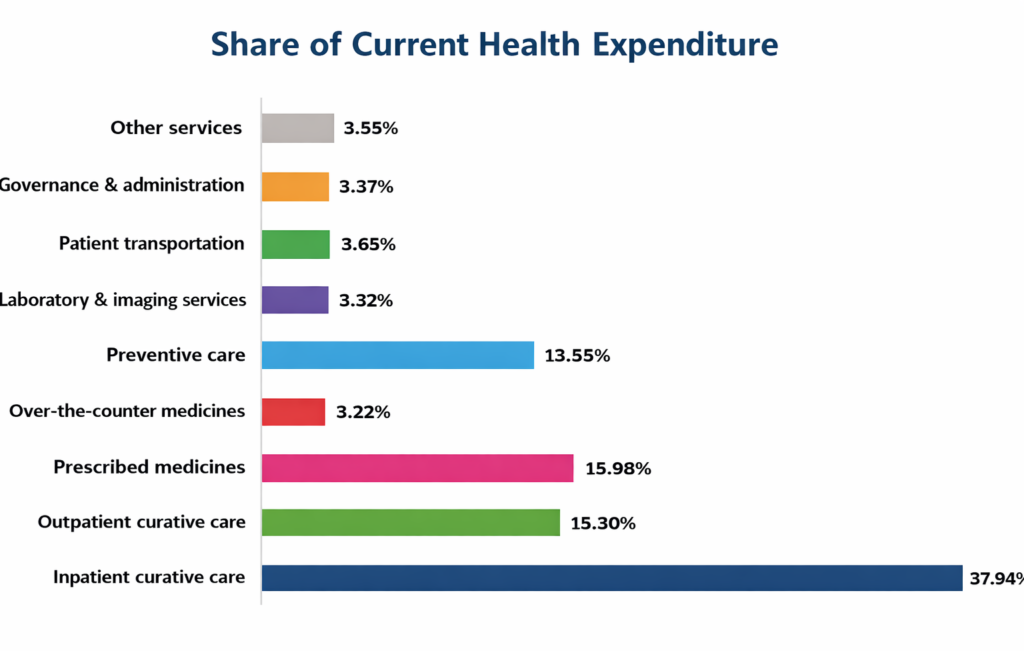

As can be observed from the graph below, inpatient curative care has the largest share in current health expenditure, at 37.94%, followed by prescribed medicines at 15.98%, outpatient care at 15.3%, and over-the-counter medicines at 3.22%. Preventive care has a share of 13.55% in total expenditure, while diagnostic services like laboratory and imaging tests have only 3.32%. Other areas, like patient transportation, administrative functions, and so on, have smaller shares. This again emphasizes that curative and pharmaceutical spending have the largest share in India’s healthcare landscape.

Sources of Health Financing in India

The financing pattern of India has been shifting gradually over the last two decades. In the financial year 2004-05, the total expenditure on healthcare from the households’ side was 69.4 percent of the total healthcare expenditure in India. The government expenditure on healthcare was just 29 percent. However, the financing pattern of healthcare in India has been shifting gradually. The data from the National Health Accounts shows that the total government expenditure on healthcare has been rising steadily. The government expenditure on healthcare has risen to 48 percent in the financial year 2021-22. The total expenditure from the households’ side has declined to 39.4 percent. This is due to the rise in the government expenditure on the implementation of major healthcare programs such as the National Health Mission and the Ayushman Bharat – Pradhan Mantri Jan Arogya Yojana (PM-JAY) program. The total expenditure from the households’ side is still a significant percentage of the total healthcare expenditure in India. This shows that the healthcare sector in India still needs to be strengthened.

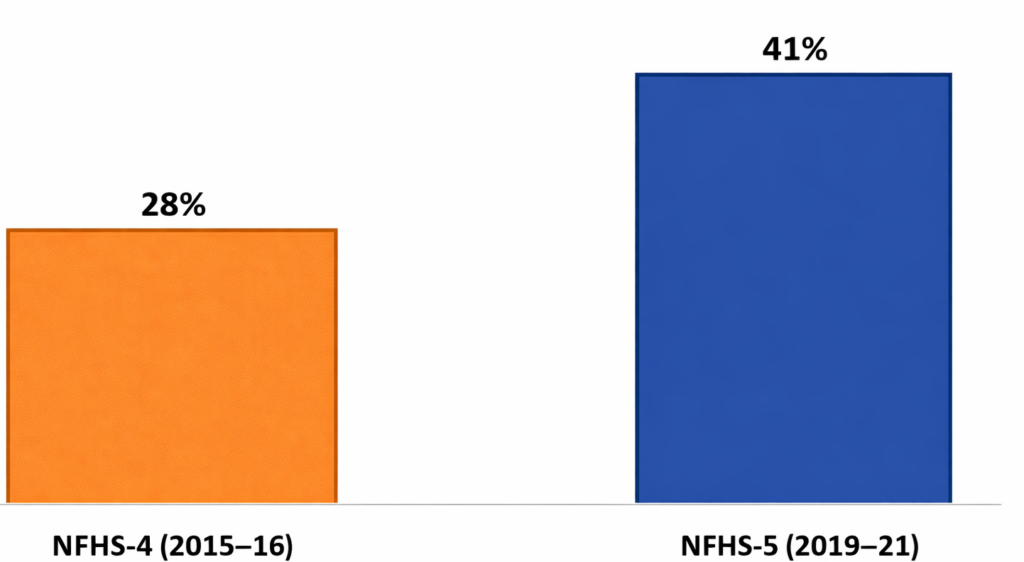

India has experienced a significant expansion in health insurance coverage in recent years. Health insurance plays an important role in sharing financial risks and protecting households from catastrophic medical expenses. Data from the National Family Health.

Survey indicate a steady rise in coverage, from 28% of the population in NFHS-4 (2015–16) to 41% in NFHS-5 (2019–21). Government initiatives have been central to this expansion, particularly Ayushman Bharat – Pradhan Mantri Jan Arogya Yojana (PM-JAY), launched in 2018. Several states have also introduced their own insurance programmes, including Aarogyasri in Telangana and Andhra Pradesh, the Chief Minister’s Comprehensive Health Insurance Scheme in Tamil Nadu, and Bhamashah Swasthya Bima Yojana in Rajasthan.Despite the expansion of coverage, the reduction in out-of-pocket expenditure remains limited. Most insurance schemes primarily cover hospitalisation, while a substantial share of household healthcare spending in India occurs on outpatient care and medicines, which are often not fully covered by insurance programmes.

The Burden of Healthcare Costs on Households

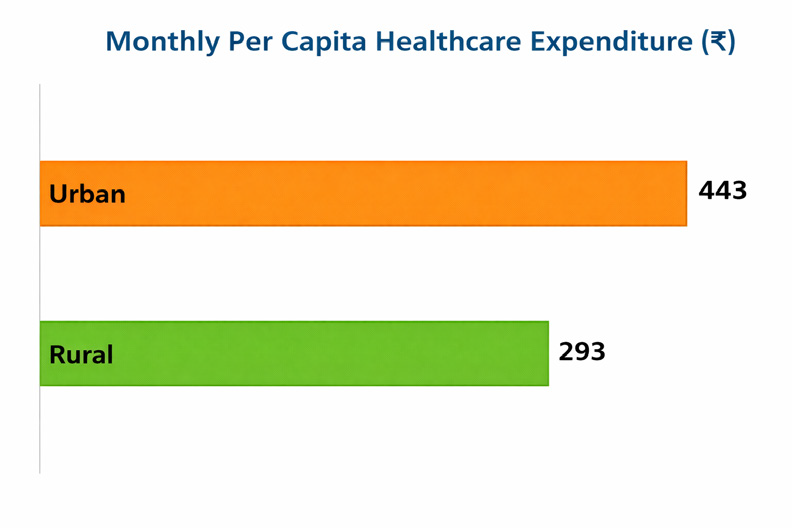

High out-of-pocket expenditure has significant socioeconomic implications for households in India. Healthcare spending constitutes an important component of household consumption expenditure and can impose considerable financial pressure, particularly among lower-income groups. According to the Household Consumption Expenditure Survey (HCES) 2022–23), the average monthly per capita expenditure on healthcare is ₹293 in rural areas and ₹443 in urban areas.

Despite improvements in public financing, out-of-pocket payments still account for a substantial share of healthcare spending. Data from the National Health Accounts (2021–22) show that 39.4 percent of total health expenditure in India is financed through out-of-pocket payments, although this share has declined from 69.4 percent in 2004–05. Strengthening primary healthcare systems is widely recognised as an effective strategy for reducing long-term healthcare costs. Early diagnosis, preventive care, and community-level treatment can reduce the need for expensive hospitalisation. Under the Ayushman Bharat program.

me, more than 1.6 lakh Health and Wellness Centres have been operationalised to expand access to primary healthcare services, including maternal and child health, screening for non-communicable diseases, and provision of essential medicines and diagnostics. In addition, the Pradhan Mantri Jan Arogya Yojana (PM-JAY) provides financial protection of up to ₹5 lakh per family per year for secondary and tertiary hospitalisation to eligible households, improving financial protection for vulnerable populations and reducing the risk of catastrophic health expenditure.

The Road to Universal Health Coverage

The foundation for Universal Health Coverage (UHC) rests upon three main principles: access to essential healthcare services, quality of healthcare services, and financial protection against healthcare costs. Hence, the reduction in out-of-pocket expenditure is essential for ensuring that people access healthcare services in a timely manner.

Significant achievements in India: India has shown remarkable improvements in UHC in the last few years. According to the National Health Accounts, the out-of-pocket expenditure as a percentage of total health expenditure in India has reduced from 69.4 percent in 2004-05 to 39.4 percent in 2021-22. The percentage of government health expenditure has increased to 48 percent. The percentage of people covered by health insurance in India has increased from 28 percent in NFHS-4 (2015-16) to 41 percent in NFHS-5 (2019-21).

Significant gaps in India: Despite the improvements in India’s UHC achievements in recent years, there still exist some gaps. Firstly, nearly two-fifths of the health expenditure in India is still spent by people. Secondly, a large percentage of healthcare expenditure in India is due to outpatient expenditure and medicine costs.

The policy priorities should therefore focus on increasing public health expenditure, extending insurance coverage to outpatient services, and improving access to affordable medicines and primary healthcare. These measures are essential in building an inclusive health system and advancing progress towards Universal Health Coverage

Conclusion:

India’s healthcare system has made significant progress over the past two decades through institutional reforms and expanded public health programmes. Initiatives such as the National Health Mission and Ayush man Bharat have improved access to healthcare services and strengthened financial protection for large sections of the population. Evidence from the National Health Accounts also shows a gradual decline in the share of out-of-pocket expenditure in total health spending, reflecting increased public investment and the expansion of government health initiatives.

Despite these improvements, important challenges remain. Household spending still constitutes a considerable share of healthcare financing, and many families continue to face financial hardship due to medical expenses. High out of pocket payments often discourage individuals from seeking timely treatment and may lead to catastrophic health expenditure that pushes vulnerable households into debt or poverty.

Achieving universal health coverage in India will therefore require sustained policy commitment. Increasing public health expenditure, expanding insurance coverage to include outpatient services, improving access to affordable medicines, and strengthening primary healthcare systems will be essential steps toward reducing the financial burden on households. Ensuring that healthcare services are accessible, affordable, and of good quality will be crucial for building a more equitable and resilient healthcare system in India.

Clear Cut Health Desk

New Delhi, UPDATED: April 13, 2026 09:00 IST

Written By: Nairita Das