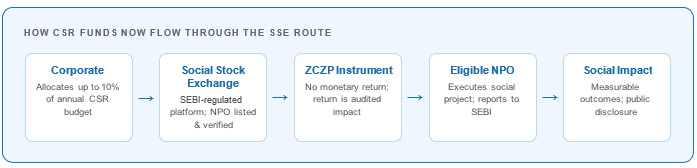

- The Government of India has amended CSR rules to allow companies to invest up to 10% of their annual CSR spending through Social Stock Exchange (SSE)-listed Zero Coupon Zero Principal (ZCZP) instruments, linking corporate funding with verified social impact projects.

- The reform aims to improve transparency, accountability, and impact measurement by directing CSR funds toward SEBI-regulated non-profit organisations that meet strict disclosure and governance standards.

- By connecting India’s ₹30,000 crore CSR ecosystem with the SSE, the amendment could create new funding opportunities for credible grassroots organisations and strengthen the country’s social development sector.

India has one of the largest mandated corporate social responsibility frameworks in the world. Since 2014, companies above a certain size have been legally required to spend at least 2% of their average net profits on social causes from education and

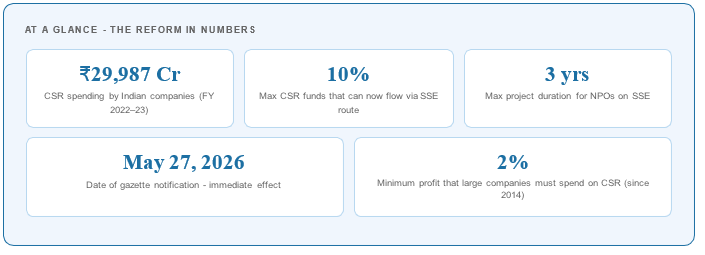

healthcare to environmental sustainability and skill development. In FY 2022-23 alone, eligible companies collectively reported CSR expenditure of nearly ₹30,000 crore.

That is an enormous pool of capital. But for years, it sat largely disconnected from a parallel experiment that India had been quietly building: the Social Stock Exchange, a regulated marketplace specifically designed to channel funds toward credible, verified non-profit organisations with demonstrable social impact.

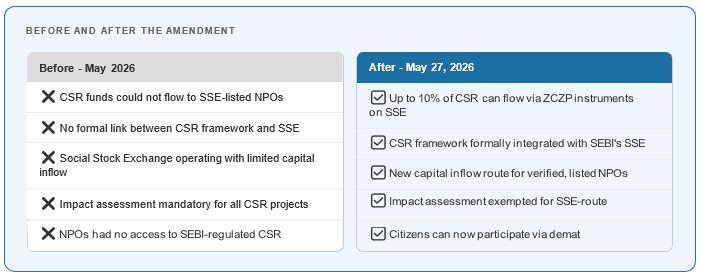

On May 27, 2026, the Ministry of Corporate Affairs notified an amendment to the Companies (CSR Policy) Rules that bridges this gap formally. Companies can now deploy up to 10% of their annual CSR expenditure through Zero Coupon Zero Principal instruments listed on Social Stock Exchanges. The reform took effect immediately.

What exactly changed and what is a ZCZP instrument?

The amended rules formally notified as Gazette Notification G.S.R. 415(E) permit companies to fulfil their CSR

obligations by subscribing to Zero Coupon Zero Principal (ZCZP) instruments issued by non-profit organisations registered on the Social Stock Exchange segment of a recognised stock exchange, in accordance with SEBI regulations.

ZCZP instruments are unlike anything in conventional finance. They carry no coupon meaning no interest is paid. They carry no principal repayment meaning the contributor does not get their money back. What they offer instead is something harder to quantify but increasingly valued: a transparent, audited, and verifiable account of social impact. The return on a ZCZP is not a dividend. It is a child enrolled in school, a well dug, a livelihood built.

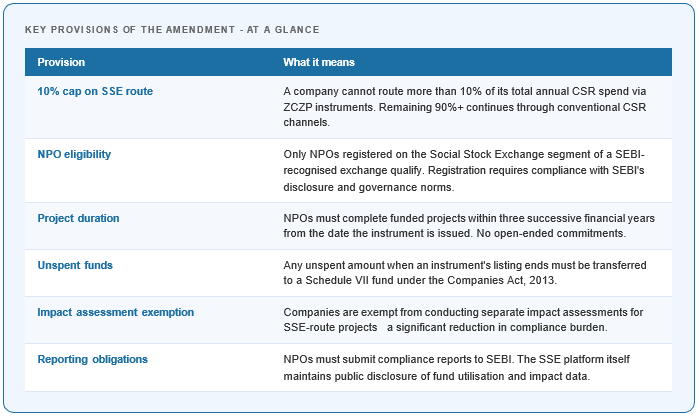

The rules : what corporates must know

The amendment is not a free pass. It comes with a precise regulatory architecture, designed to ensure that the SSE route is used with discipline rather than as a compliance shortcut.

Why the Social Stock Exchange was built and why it struggled

The Social Stock Exchange was not a sudden idea. SEBI introduced the framework in 2021 after a high-level working group recommended a regulated platform where social sector organisations could raise capital with the same rigour expected of listed

companies. The intent was to solve a persistent problem: India had thousands of non-profits doing credible, measurable work in education, health, gender equity, and livelihoods, but they operated in a fragmented and largely unregulated funding environment where due diligence was inconsistent, and impact reporting was rare.

The SSE required listed organisations to meet strict registration criteria, publish Social Impact Assessment reports, disclose fund utilisation publicly, and adhere to governance standards. It was, in essence, a bid to professionalize philanthropy.

But the exchange faced a structural problem. India’s largest organised pool of social capital mandatory CSR spending was not permitted to flow through it. The bridge existed. The traffic did not. May 2026 amendment changes that by opening the SSE to CSR funds for the first time.

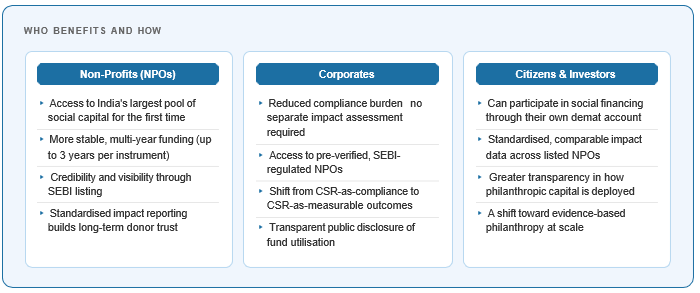

Who stands to benefit and how

For the development sector, the significance of connecting CSR capital with a regulated impact marketplace cannot be overstated.

For years, the conversation in India’s social sector has been about the quality of funding as much as the quantity. Grants that

arrive late, tranches that disappear without explanation, impact reporting that is performative rather than rigorous these are persistent frustrations for grassroots organisations doing credible work.

The SSE model, at least in theory, addresses these structural problems. NPOs that list on the exchange have agreed to disclose. Their projects are public. Their fund utilisation is traceable. Their social impact claims are required to meet SEBI’s Social Impact Assessment standards. For a corporate looking to direct CSR funds responsibly, this is a significantly more credible mechanism than the existing landscape of unverified implementing agencies.

What this means for India’s development sector

The reform lands at a moment when India’s development sector is under pressure from multiple directions. International funding

historically a major source of support for advocacy-focused non-profits has been tightening under FCRA restrictions.

Domestic philanthropy, while growing, remains concentrated in a few large foundations and high-net-worth individuals. The mandatory CSR ecosystem is large but fragmented, with many companies directing funds to their own foundations or to a small set of well-networked implementing agencies.

The SSE route, if it gains traction, could open a more democratic channel one where a verified tribal education organisation in Jharkhand or a community health initiative in Rajasthan could access the same corporate CSR pool as a large, well-resourced urban NGO, provided it meets the listing and disclosure standards.

The bigger picture a shift in how India funds social change

India’s CSR mandate unique globally in its scale and statutory basis has always been a blunt instrument. Requiring

companies to spend on social causes guaranteed volume but not quality. The Social Stock Exchange, now formally connected to that capital pool, is an attempt to add rigour, transparency, and outcome-orientation to the equation.

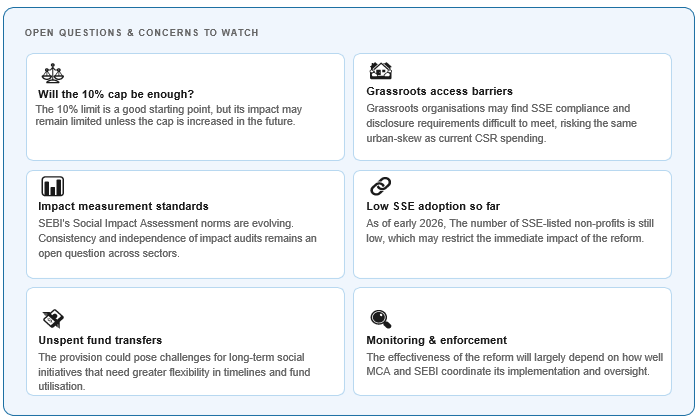

Whether it succeeds depends on how many NPOs find the listing process accessible, how many corporates choose the SSE route over more familiar channels, and whether SEBI’s impact reporting standards develop enough credibility to drive genuine allocation decisions rather than box-ticking.

But the direction is clear. India is moving slowly, through the grammar of gazette notifications and regulatory amendments toward a model where social funding is not just mandated but measured. Where the question is not only “how much did you spend?” but “what did it actually change?”

The Social Stock Exchange has been called India’s most important social sector reform in a decade. That claim will be tested in

the months ahead, as the first ZCZP instruments are subscribed under the new rules and the first impact reports come in. For now, the gate is open. The question is whether the traffic follows.

Clear Cut Research, Livelihood Desk

New Delhi, UPDATED: June 04, 2026 01:00 IST

Written By: Shivangi Mishra